Blockchain Networks Embrace Circle’s ‘Bridged USDC Standard’

The standard was designed to enhance cross-chain functionality and mitigate the issues arising from the liquidity fragmentation of USDC stablecoin.

The standard was designed to enhance cross-chain functionality and mitigate the issues arising from the liquidity fragmentation of USDC stablecoin.

In November last year, Circle, the issuer of the USDC stablecoin, introduced a new bridged USDC standard aimed at enhancing the convenience of using USDC across multiple blockchains and addressing issues related to liquidity fragmentation.

Due to the rapid increase of new blockchain networks, Circle found it increasingly challenging to integrate its native USDC quickly enough. Consequently, many of these emerging networks began adopting synthetic versions of USDC created by various third parties. This complicated the native USDC reintegration process once these synthetic USDC versions gained significant traction.

The newly launched standard was crafted to allow the use of synthetic USDC while simplifying the subsequent integration with native USDC.

Since the announcement, the standard has been widely adopted, indicating strong demand. For instance, in July, Oasys, a blockchain with a gaming focus announced a collaboration with bridge provider Celer to support this standard on its network. Similarly, the Fantom network, with assistance from Wormhole, has also integrated the standard. It has been adopted by several smaller networks as well, including Qtum, Neutron, and Kroma.

Blockchain networks need stablecoin liquidity, particularly when it comes to large and well-established stablecoins. Since Circle has said that integrating the new standard is the first and necessary step to achieving its native stablecoin liquidity, it is unsurprising that projects have begun to adopt it.

In terms of deploying native USDC, Circle has expanded its offerings this year, launching on zkSync, Polygon, and Celo. Although the number of native USDC integrations lags behind those adopting the new standard, this is not unexpected. Circle considers native integrations primarily for networks that have demonstrated substantial growth and traction.

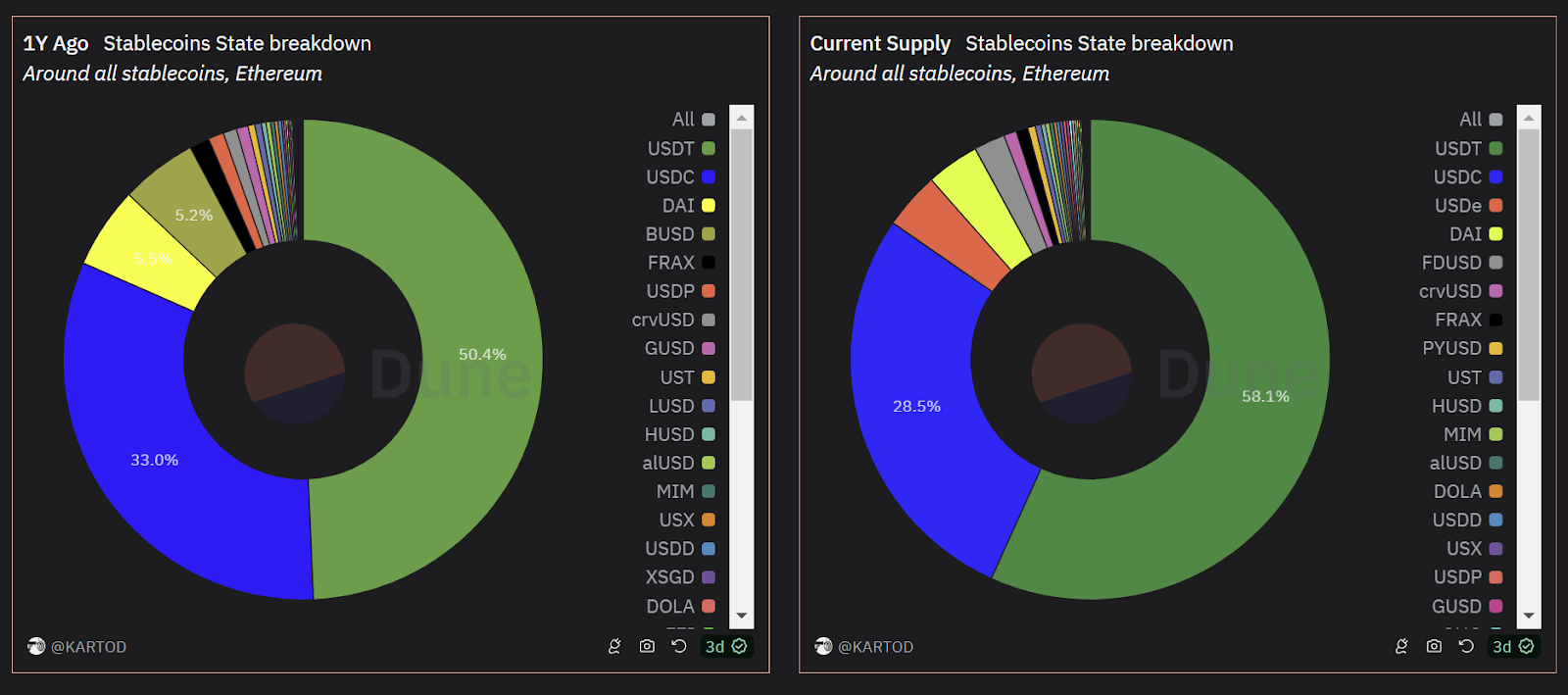

Despite these efforts, Circle’s share has diminished over the past year from a market supply perspective. From representing around 33% of the stablecoin market a year ago, USDC now accounts for 28.5%. Meanwhile, USDT, another major stablecoin, has increased its market share to approximately 58%.

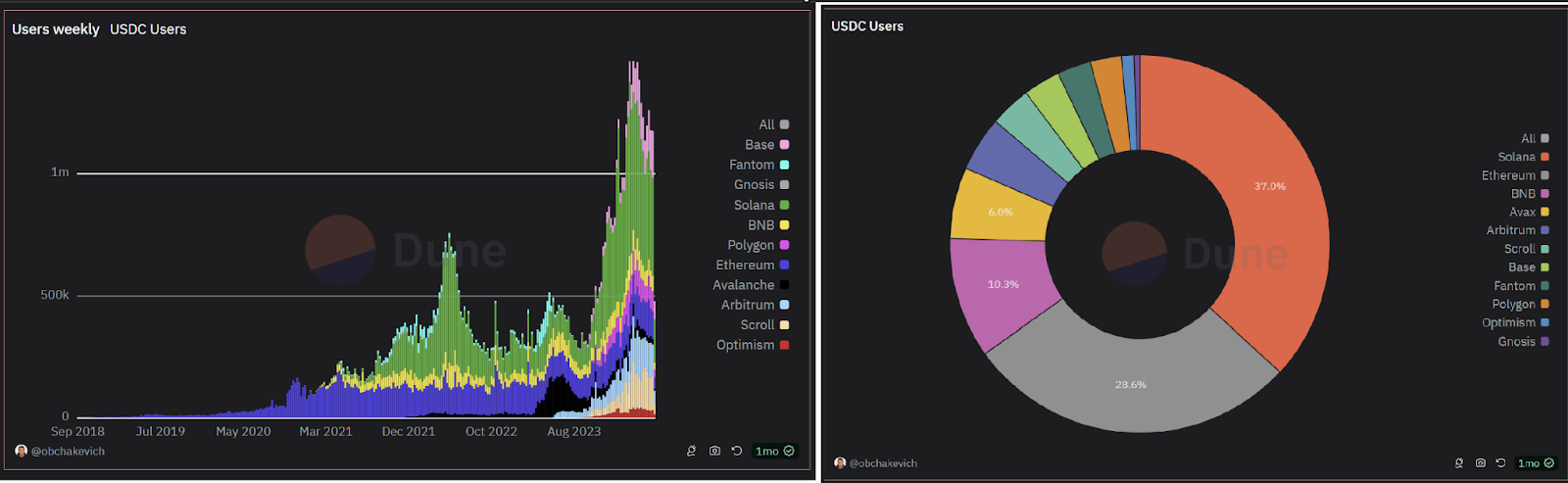

However, from a usage standpoint, USDC has exhibited significant growth, nearly doubling its user base since the beginning of the year, now servicing over one million users weekly. This uptick in usage has been particularly pronounced on the Solana chain, fueled by the memecoin frenzy, where USDC has become the principal stablecoin.

In comparison, USDT maintains a larger user base of approximately 5-6 million weekly users, predominantly on the Tron blockchain.

Undoubtedly, USDC and USDT remain the largest and most widely used stablecoins in the space, and new integrations help expand their dominance. Nevertheless, we are witnessing new entrants that could potentially challenge these established stablecoins. Projects like Ethena and Usual are good examples of this.

However, this competition will likely take time to materialize, and in the short to medium term, there will likely be no significant changes in the competitive landscape of stablecoins.