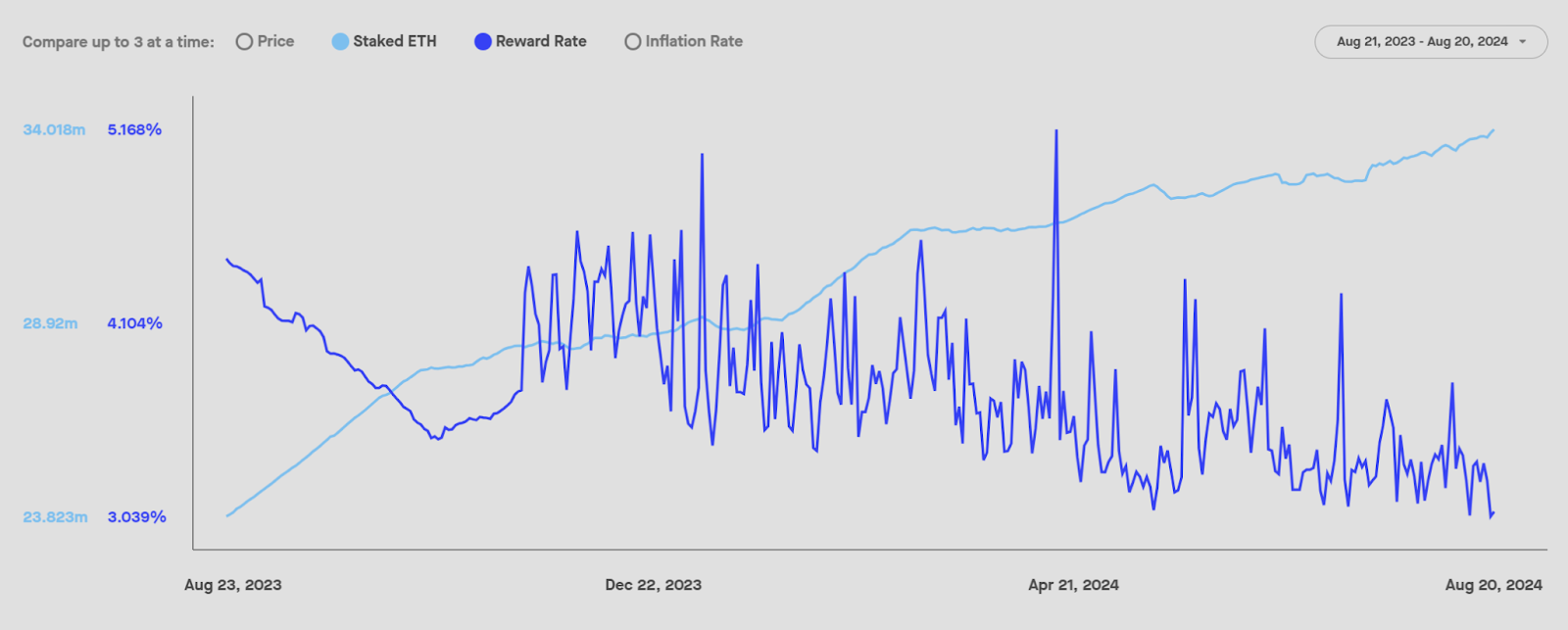

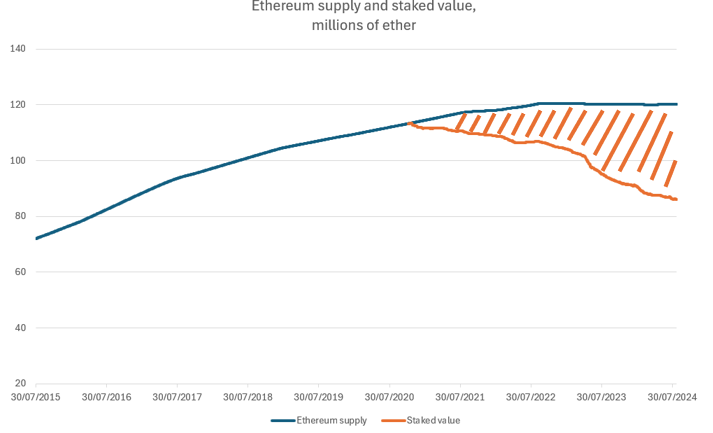

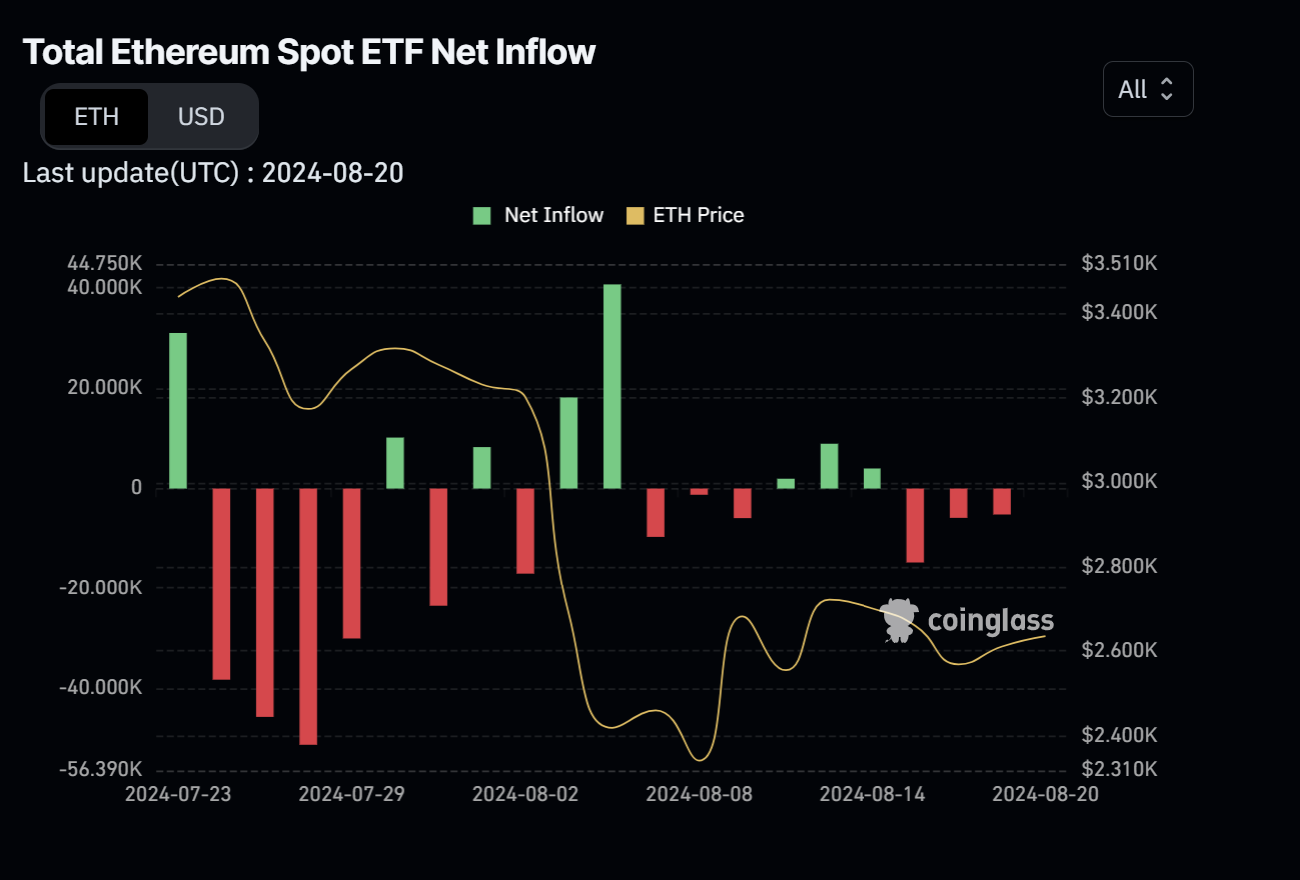

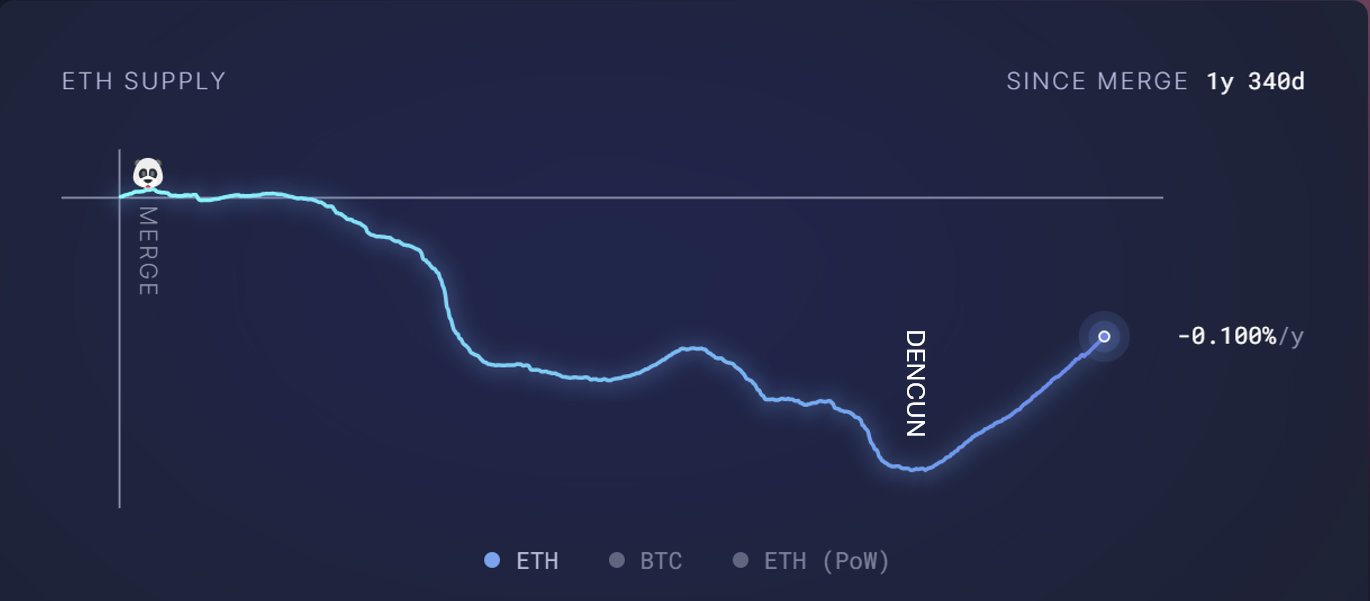

Locking Crypto Doesn't Help Price: Ethereum's Case

The ratio of staked Ethereum is growing consistently, yet it does not affect the token's price. Speculative markets and short-term sentiment seem to have more say in the price discovery of crypto with little monetary utility