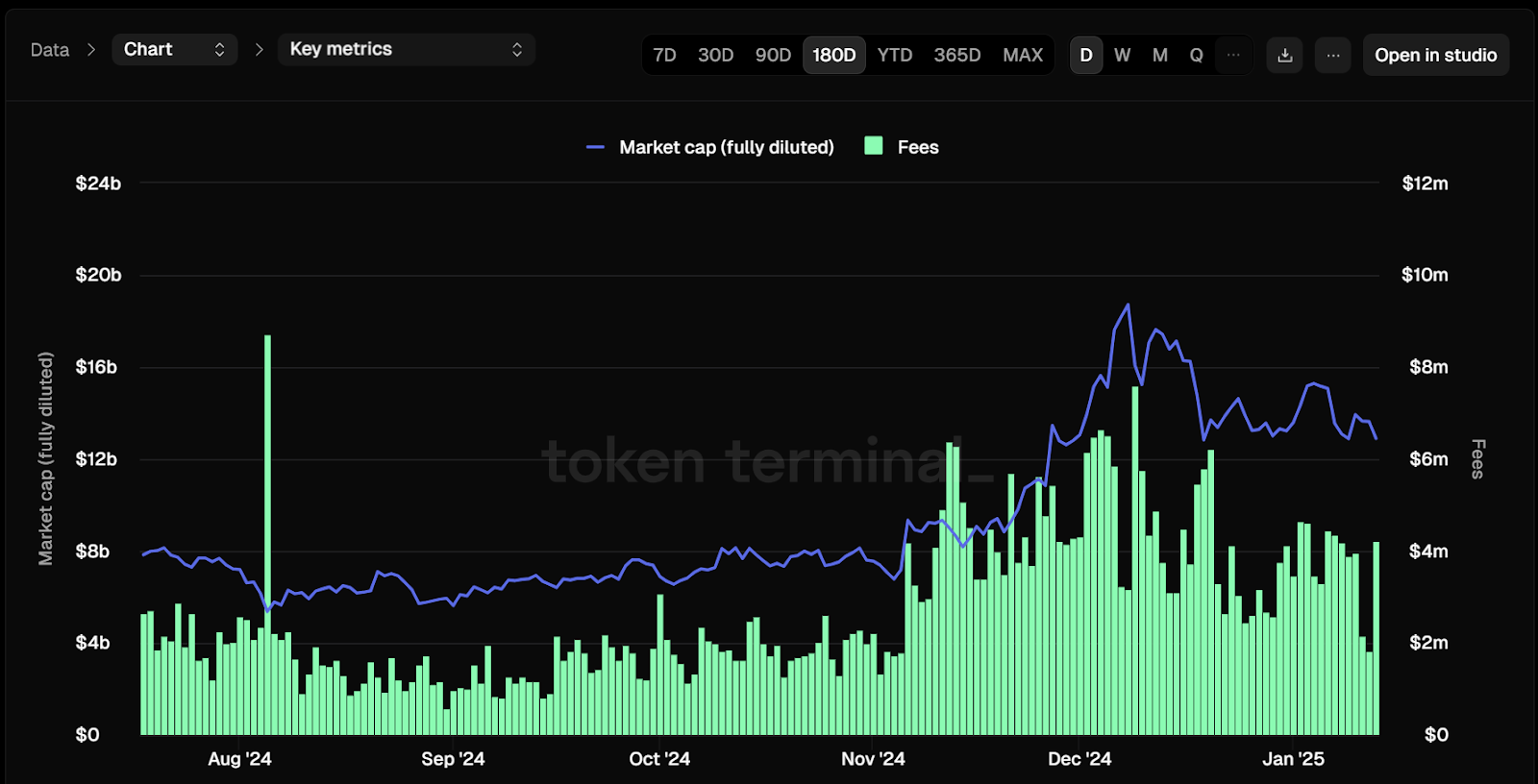

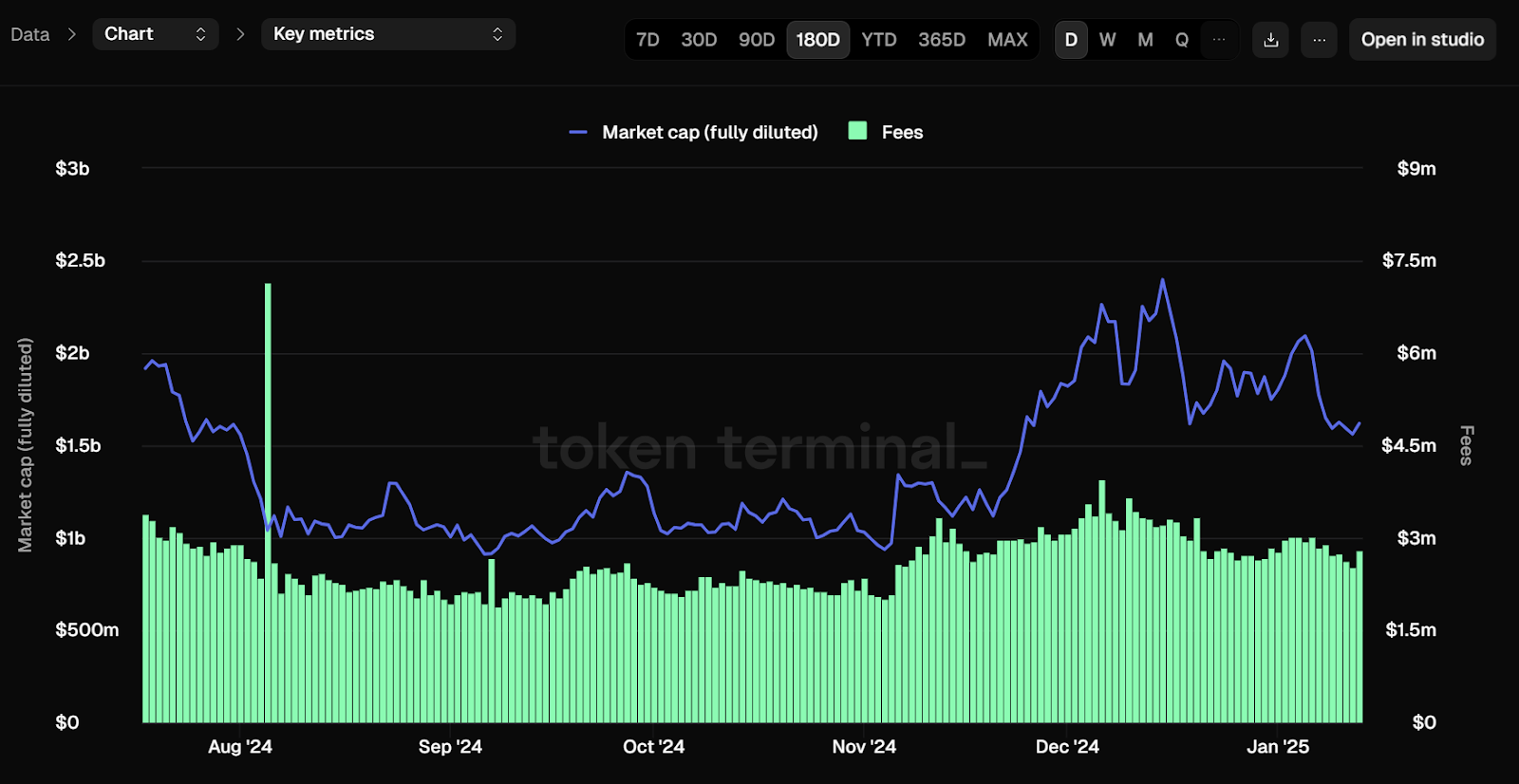

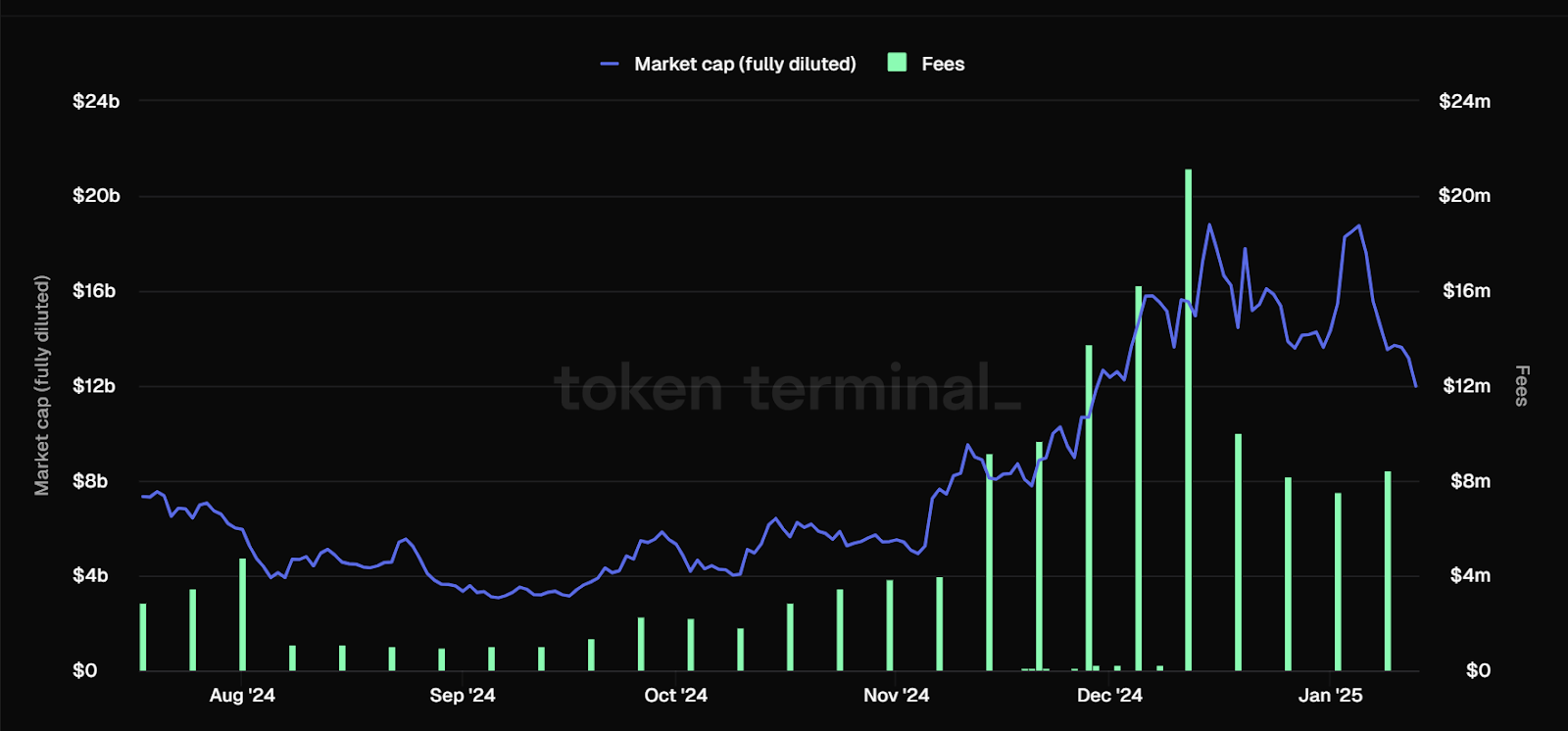

Money, Stock, or Maybe... Nothing. What Is the Value of a Governance Token?

DeFi projects are increasingly planning to share revenue with token holders, making these tokens similar to traditional dividend-paying shares. This trend suggests that DeFi may begin to resemble traditional finance systems while maintaining its decentralized nature.