Wildcat Banking Lasted For 30 Years. How Long Does Wild Crypto Have?

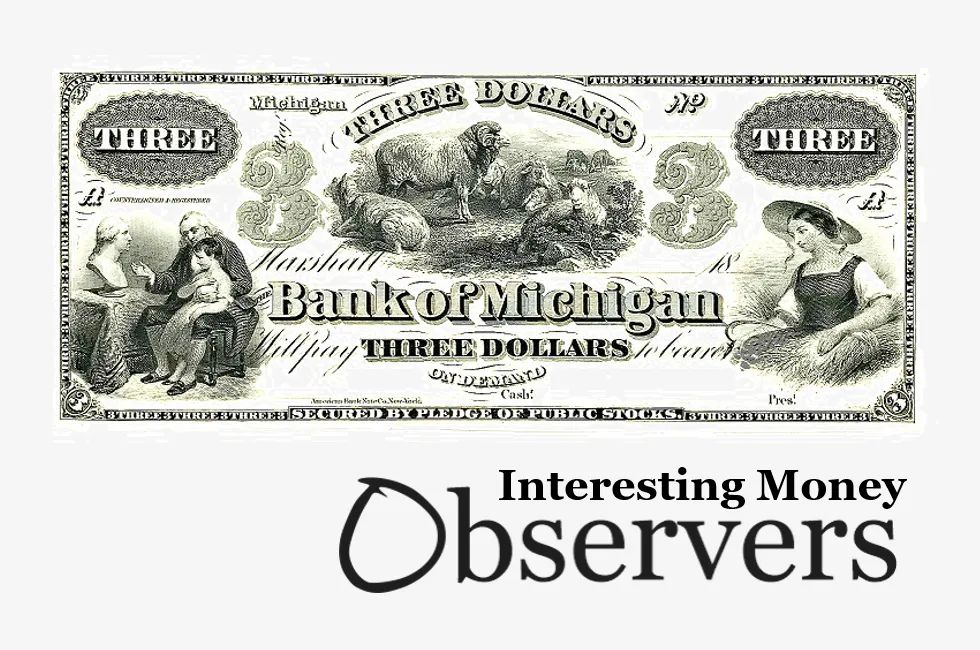

The evolution of stablecoins mirrors that of Wildcat Banking: a period of non-federal regulation over the monetary system in the U.S. during the 19th century.

The evolution of stablecoins mirrors that of Wildcat Banking: a period of non-federal regulation over the monetary system in the U.S. during the 19th century.